A currency-issuing government is not revenue constrained. It is always able to purchase whatever is available for sale in its own currency. This simple reality is partially concealed by a variety of contrived hoops through which modern day governments require themselves to jump. There are at least two different ways in which we can see past the confusion. The easiest way is to stand back and look at the big picture, both from the standpoint of logic and by considering the monetary and fiscal authorities as two parts of the same entity, the consolidated government sector. For the eagle eyed, this approach may appear to overlook potentially consequential details in the way governments actually spend. In practice, the monetary authority plays one set of roles, the fiscal authority plays another, and many governments have introduced various restrictions on the way in which the two can interact. The present post begins with a bird’s eye view of government spending, and then turns to a more detailed consideration of the way in which self-imposed constraints and convoluted operational procedures complicate but do not undermine the sovereignty of a currency-issuing government. The case of the US government is taken throughout as an example, but much of the discussion is also broadly applicable to other currency-issuing governments.

A basic point of logic

As a simple matter of logic, a currency-issuing government that imposes a tax denominated in its own money cannot receive tax payments until it has first issued that money. Likewise, it cannot borrow its money from the non-government without first having issued money. A currency-issuing government creates money when it spends or lends. Tax payments and purchases of government bonds result in the destruction of money. This makes clear, as a matter of first principles, that government spending or lending must occur before tax payments or government borrowing can take place.

In fact, we can be more precise than this. It is only government spending that enables non-government to fulfill its financial obligations to the state. Mostly, when central banks advance government money to non-government (specifically, banks), it is on the condition that non-government supplies collateral in the form of government bonds. The bonds used as collateral only exist because of past government spending. Therefore, when such a condition is in force, it is government spending that comes first. Even in the case of an uncollateralized overdraft on a bank’s reserve account, which will attract a penalty, this leaves non-government liable to repay the loan. As such, a government loan to enable a tax payment merely turns the tax liability into a loan liability. For non-government as a whole, the financial obligation created by the imposition of the tax can only be eliminated once government has spent.

The US government, for example, requires taxes to be paid in dollars. To the extent the government spends more than it taxes, the fiscal authority (Treasury) sells government bonds to non-government. Both tax payments and purchases of government bonds are settled via Fedwire when the monetary authority (the Fed) debits the appropriate reserve accounts. Reserves are a form of government money. They are a liability of the Fed and asset of the banks. For taxes to be paid, or government bonds to be purchased, there must be sufficient reserves in the system. If there are not, the Fed will need to do a ‘reserve add’ by lending to non-government. Since the Fed requires the recipients of the loan to provide collateral in the form of government bonds, and government bonds are the result of past government spending, it is government spending that comes first in the US system, as is the case in other sovereign currency systems.

The consolidated government sector

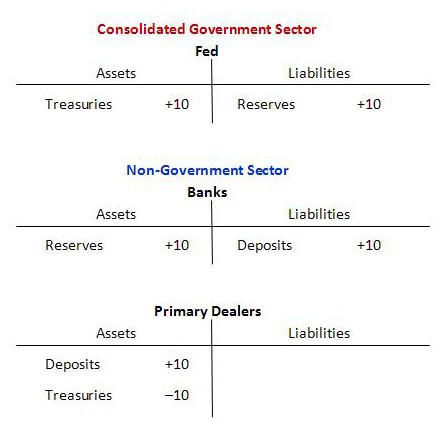

Often, when we are analyzing the economy as a whole, it is convenient to ignore the distinction between the monetary and fiscal authorities and simply consider them as part of a consolidated government sector in which Congress and the President are at the top of the hierarchy and the Fed and Treasury are their agents. This is fine for many purposes, because internal interactions between different parts of government have no impact on non-government. What matters to non-government is the combined effect of the consolidated government sector’s operations.

When viewed in this bird’s eye way, the overall effect of government spending and borrowing is easy to see. Government spending, considered in isolation, results in the creation of extra reserves. The recipients of the government spending end up with additional balances in their bank accounts. However, if government net spending is matched by bond issuance, the overall level of reserves is ultimately unaffected because some members of non-government purchase bonds matching the amount of the government spending and this, considered in isolation, drains reserves. In aggregate, total reserves remain unchanged, but there is an increase in net financial assets, held in the form of government bonds. It is as if the government spends, adding reserves, and these extra reserves are exchanged for bonds.

Distinguishing between the Fed and Treasury

The bird’s eye view of government spending is fine for most purposes. But if we want to understand the way in which government spending actually occurs under current practices, and confirm that these operational details do not diminish currency sovereignty, it is necessary to peer inside the consolidated government sector. In particular, we need to separate out the actions of the Treasury and Fed and consider the consequences for their respective balance sheets.

Many governments have put in place various self-imposed constraints on their own operations that require them to engage in a more circuitous (and inefficient) series of actions to achieve the same ultimate effect as could be obtained simply by crediting reserve accounts and exchanging them, if desired, for government bonds. Two self-imposed constraints have been prominent in the US:

- The Treasury is required to keep an account with the Fed and to draw upon that account when it spends;

- The Treasury is forbidden from borrowing directly from the Fed (that is, the Fed is not permitted to buy bonds directly from the Treasury but must instead obtain them in the secondary market).

At first glance, these constraints might seem problematic. We know as a matter of logic that government spending is required before the non-government’s financial obligations to the state can be extinguished or government bonds can be purchased. But due to the self-imposed constraints, the Treasury needs balances in its account at the Fed before it can spend and cannot get them directly from the Fed. This makes it appear as if the government is not a currency sovereign at all. It seems as if the government depends on non-government to obtain the dollars it spends. It creates the illusion that the government could be forced into involuntary insolvency, unable to pay its debt, or fall victim to the bond vigilantes. Yet, we know that this is a logical impossibility for a currency-issuing government.

To resolve the apparent contradictions, we need to look more closely at the operations involved. It will help if we have a specific scenario in mind. Suppose the Treasury intends to spend but has a zero balance in its account at the Fed. Suppose, also, to make the situation as “difficult” as possible for the government, that there are initially no funds available in the Treasury’s ‘tax and loan’ accounts, which are held at various banks and can be called in to the Treasury’s account at the Fed. Suppose, lastly, that banks presently hold the quantity of reserves that they wish to hold, and so do not currently desire to convert some of their reserves to bonds.

This gives us the following situation. The Treasury is only allowed to spend by drawing down its account, but the account is empty. Its tax and loan accounts are also empty. The Treasury is not permitted to borrow directly from the Fed. Evidently, the Treasury will have to auction off bonds to primary dealers or other members of non-government. And it will have to do this before the next act of government spending. But it has also been specified that banks are currently holding the quantity of reserves that they desire, and have no present intention to convert some of their reserves into bonds.

We might wonder, then, where the reserves will come from that are required to settle the Treasury auction? The answer is that they will come from the Fed. The Fed will have to do a reserve add, by lending to non-government, specifically to primary dealers. In doing so, the Fed will require primary dealers to supply collateral in the form of government bonds. The bonds used as collateral only exist because of prior rounds of government spending.

So the first step, before the Treasury issues new bonds, and before primary dealers purchase the bonds, involves the Fed doing a reserve add, which as currency issuer it can do without limit. In short, the Fed lends to primary dealers, who are required to participate in the process. The Fed advances reserves, requiring government bonds as collateral. The collateral will be returned upon repayment of the loan in the second leg of a so-called repurchase agreement or ‘repo’, which will be timed to offset the effect on reserves of government spending (which, when it occurs, involves the crediting of reserve accounts). But in the first leg of the repurchase agreement, the Fed credits the reserve accounts of the primary dealers’ banks and directs the banks to credit the primary dealers’ accounts. The resulting surplus of reserves incentivizes a conversion of the excess into bonds.

This makes clear why there is no danger of a lack of demand for government bonds at the Treasury auction. The Fed has created additional reserves, which earn zero or little interest. Agents would prefer to receive more interest than is paid on reserves, and so form a ready market for government bonds. It is equally apparent that market participants have no capacity to pressure the Treasury into offering an interest rate that is much higher than it wishes (for policy reasons) to pay. The choice for non-government agents is between reserves that pay little or no interest and government bonds that pay somewhat higher interest. In any case, if the central bank feels it necessary, it can purchase assets in the secondary market without limit, putting downward pressure on interest rates and exerting downward influence on the cutoff bid at the Treasury auction.

So, as logic had already dictated, government spending must occur before financial obligations to the state can be settled or government bonds purchased. The way the operations are arranged makes it appear as if it is government lending that comes first. But as has already been noted, this is not actually the case. While central bank lending is the first step in the current round of spending, the government bonds that the banks must supply as collateral only exist because of previous government spending. So, it is actually government spending that comes first. It is just that the government spending that created the bonds occurred during an earlier round of spending.

It is worth noticing that the very first time the government spent it could not have used this roundabout process, because it would have been impossible for primary dealers to supply government bonds as collateral. From inception, the currency will be issued either by the government spending or the central bank lending without requiring government bonds as collateral. Needless to say, it would be foolish for the government to take the latter option. From inception, the government will issue the currency by spending. It is only once the system is up and running that the more roundabout method can be introduced. It is presumably introduced for deceptive purposes. It misleads many in the general public into believing that a currency issuer can somehow run out of what it alone can issue. It creates the illusion that the currency issuer is revenue constrained when in actuality it is only constrained by real resources and politics.

Monetary and fiscal operations when the US government spends

It is possible to trace through the sequence of operations that are involved when the US government spends. In normal times, when there is neither quantitative easing nor interest on reserves and the Fed is targeting a positive short-term interest rate, there are six basic steps in the process. The following description is based on a post by Randall Wray and a freely downloadable academic paper by Scott Fullwiler. The six steps are as follows:

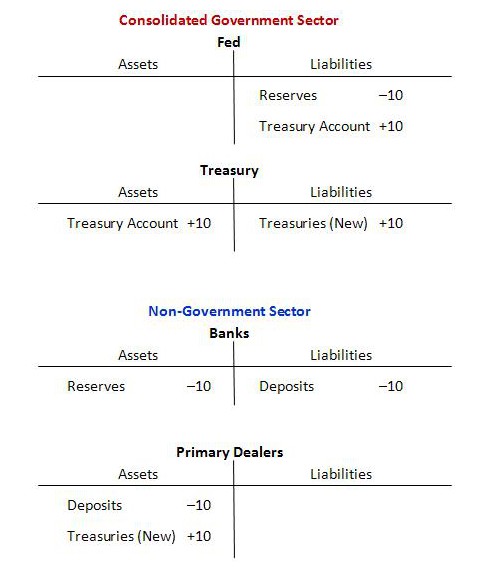

1. Repurchase agreement. The Fed credits reserve accounts and instructs the banks to credit the accounts of the primary dealers (the primary dealers mostly are banks) while requiring government bonds as collateral. This step, like later ones, can be represented in T-accounts. (A more sophisticated approach is taken by Fullwiler in the paper linked to above.) It is arbitrarily assumed in the T-accounts that the amount of government spending involved is 10 (million, or perhaps billion) dollars. The repurchase agreement has effects on the T-accounts of the Fed, banks and primary dealers, but the overall impact on net financial assets is zero, since the step just involves an asset swap.

2. Treasury auction. New bonds are offered to non-government. For simplicity, we can assume they are purchased entirely by the primary dealers, but in general that need not be the case. For present purposes, this simplifying assumption makes no meaningful difference to the analysis. The auction will involve a depletion of reserves as primary dealers draw down bank accounts to pay for the bonds, and will add balances to the Treasury’s account at the Fed. The action in this step affects the T-accounts of the Fed, the Treasury, banks and primary dealers. As with the first step, overall there is no impact on net financial assets.

3. Deposits in tax and loan accounts. The Treasury adds the balances received as a result of the Treasury auction to its tax and loan (T&L) accounts held at various banks. This action therefore adds both to deposits held at banks and reserve account balances. There will be effects on the T-accounts of the Fed, the Treasury and banks. Here, too, the overall effect on net financial assets is zero.

(NB. Steps 4 and 5 can occur in reverse order without consequence.)

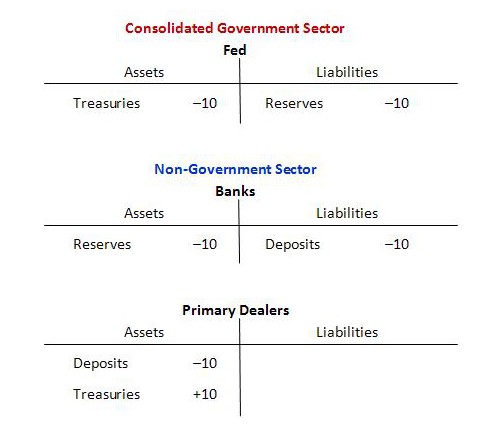

4. Second leg of the repurchase agreement. This reverses step 1. Primary dealers receive back the bonds that were supplied as collateral in step 1 upon repayment of the loan, which involves a debiting of reserve accounts. The T-accounts of the Fed, banks and primary dealers will be affected. Since this is just the reverse of the prior asset swap, the overall impact on net financial assets is zero.

5.The Treasury calls in tax and loan balances ready to spend. This reverses step 3. There is a depletion of deposits held at banks and in reserve accounts, and effects on the T-accounts of the Fed, the Treasury and banks. Once again, the overall impact on net financial assets is zero.

6. The Treasury spends. The Treasury spends by drawing down its account at the Fed, resulting in a crediting of reserve accounts and a crediting of the bank accounts of spending recipients. The T-accounts of the Fed, the Treasury, banks and spending recipients will all be affected. Net financial assets increase by the amount of the government spending.

As mentioned earlier, the aggregate level of reserves remains unchanged as a result of steps 1 through 6. The increase in deposits for spending recipients is offset by a depletion of deposits held by the purchasers of bonds. Even so, non-government as a whole is better off. This is made clear by the fact that total deposits are unchanged but holdings of government bonds have increased. The effect of the government spending, as expected, is to increase net financial assets by the amount of the spending. A summary of the entire 6-step procedure is shown below.

The vertical sums in the bottom row of the table show that: (i) the Fed’s assets and liabilities remain unchanged as a result of the operations; (ii) the Treasury has unchanged assets but an additional liability equal to the new issue of bonds in step 2; (iii) the consolidated government sector as a whole has created an additional liability equal to the new issue of bonds; (iv) the assets and liabilities of the banks and primary dealers remain unchanged as a result of the operations; (v) the assets of the spending recipients have increased by the amount of the extra balances in their accounts; and (vi) the increase in net financial assets of non-government equals the change in debt of the consolidated government sector, as it must by definition.

The horizontal sums in columns 6 and 13 of the table show that only the final step in the 6-stage procedure has any net impact on the financial positions of the consolidated government and non-government sectors. The net impact is equal to the reserve add in step 6, which is of the same magnitude as the issue of new bonds in step 2. As we had already discerned on the basis of a bird’s eye view, it is as if the government spends and the newly created reserves are exchanged for bonds. However, the first part of the swap is done earlier, in step 2, enabled by the Fed’s reserve add in step 1. This is only possible because government spending of previous rounds has resulted in a sufficient supply of government bonds to execute the swap.