In recent exchanges on Marx and MMT, one question has concerned the capacity of government spending to encourage private investment and promote employment. Some Marxists appear to regard MMT as incompatible with Marx on this question. My own view is that Marx and MMT are compatible, both in general and on this particular question, and that the contributions of both, when viewed together, hold an important long-term social implication. What follows is a set of remarks outlining my position. Remark 1 is intended to provide context and to identify what I regard as the main social implication following from a joint reading of Marx and MMT. Remark 2 notes the critical significance of Marx’s ‘law’ of the tendential fall in the profit rate when interpreting the long-term implications of MMT from a Marxist perspective. Remarks 3 to 10 concern private investment under capitalist conditions, its likely responsiveness to government spending, but also its crisis prone nature. Remark 11 questions the appropriateness of society pinning its future aspirations on private investment behavior. It is suggested that a transition to socialism is both preferable and, on the basis of MMT, already technically feasible for societies with their own currencies.

Remark 1 – Context and social significance

In at least one important respect, there may be less disagreement between Marxists and MMTers than might initially seem the case. If Marx’s law of the tendential fall in the profit rate holds, then on the basis of MMT there are ultimately two ways to approach policy. Either: (i) move more activity outside the sphere of commodity production (whether to the public sector, to the proposed job-guarantee sector, or to the non-government not-for-profit sector); or (ii) permit a periodic collapse in capital values, through crises, as and when necessary to revive the rate of profit, while sheltering directly affected workers in the job-guarantee sector. MMT in itself is neutral on the path to be chosen. Both paths are compatible with it.

For what it’s worth, (i) is my preferred approach, and the choice has never seemed clearer in view of our current predicament. It is unlikely that our present challenges – a looming ecological crisis amid extreme inequalities, social divisions, and geopolitical tensions – can be overcome through a reliance on profit-seeking activity. The necessary shifts in production and consumption, if they are to be achieved at all, let alone equitably, will require coordinated action and routine overriding of profit criteria.

Remark 2 – The key significance of Marx’s profit-rate ‘law’

On the basis of Remark 1, a key question in assessing the long-term implications of Marx and MMT is the status of Marx’s profit-rate law. For the law to hold, Marx’s theory must be interpreted in a temporal single-system way. If such an interpretation is rejected, there will appear to be more policy options than the ones considered here.

When Marx’s theory is accepted and interpreted in a temporal single-system manner (which, in my view, is the most appropriate interpretation, because it maintains internal consistency, replicating Marx’s key results and conclusions starting from stated premises), then the profit-rate tendency applies, and the long-term policy choice is between a transition to a system based on directly social labor (option (i) above) or a continuation of crisis-prone capitalism (option (ii)).

Marx’s profit-rate law, however, does not contradict MMT. Although MMT indicates that a currency-issuing government can always command resources that are available for sale in its currency, this does not necessarily mean that the government can always do this in a way that is both profitable to capitalists and averts crises. If Marx’s profit-rate law holds, ultimately we will need to choose (i) or (ii).

Remark 3 – Necessary and sufficient conditions for private investment

The question of whether Marx’s profit-rate law holds is important when it comes to a consideration of the long-term behavior of private investment. I’ll state my view of private investment behavior in a nutshell, then elaborate in ensuing remarks. My view, while compatible with MMT, is not the only view compatible with the framework.

Briefly, a necessary condition for private investment to occur is that the normal rate of profit r (the rate that would apply when productive capacity is utilized at the intended or normal rate) is above some minimum rmin deemed acceptable by capitalists. This, however, is not sufficient. The expectation that at least a minimally acceptable rate of profit can be generated in production will not induce private investment if firms do not expect this rate of profit to be realized in exchange. Unless there is adequate demand, the rate of profit generated in production will not be realized. Sufficiency requires both a minimally acceptable normal rate of profit and adequate demand.

In my view, so long as r exceeds rmin, private investment is ‘demand driven’ (in a sense to be explained in the next remark). The rationale for this behavior is a competitive onus on firms to expand production in response to persistently rising demand not only through higher utilization of existing capacity but through investment in new capacity whenever the normal rate of profit is deemed acceptable by competitors. Not to invest when faced with persistently strong demand and r in excess of rmin would be to risk losing market share to rivals who do invest.

This is not to downplay the priority of profit in capitalist investment decisions. Profit is the overriding aim of such investment, and a precondition for it. The supposed demand-led investment behavior is predicated on a normal rate of profit acceptable to capitalists. If the normal rate of profit (averaged over all firms) falls below the minimum level necessary to induce private investment, there will be a collapse in private investment as those firms not able to realize at least rmin cease investment.

A recovery in private investment will then require a revival in the normal rate of profit through a collapse in capital values. Capital devaluation boosts the normal rate of profit applying to new investments, and is a necessary condition for a recovery in private investment once r falls below rmin. The other necessary condition is adequate demand. As already emphasized, sufficiency requires both conditions to be met.

Remark 4 – Description of a demand-led private-investment process

What follows is a description of a demand-led private-investment process, predicated on a normal rate of profit acceptable to capitalists. It is assumed that the economy remains within ultimate capacity limits at all times and that firms can draw upon reserves of unemployed and underemployed workers as needed, reserves that are continually created and re-created through technical advances and productivity improvements. Ultimate capacity limits are respected due to the existence of planned margins of spare capacity. While firms intend, on average, to operate capacity at a ‘normal’ rate of utilization, the intentional maintenance of spare capacity enables them to expand production at more or less stable prices to meet unexpected peaks in demand through a fuller utilization of existing capacity. However, if demand is such that firms find themselves persistently operating above the normal rate of capacity utilization, they will have reason to accelerate investment in an attempt to adjust capacity to demand and restore their desired margins of spare capacity.

For private investment to be considered demand led in this manner, there needs to be an independent source of demand, specifically autonomous demand that does not directly create private-sector for-profit productive capacity. This category of spending is sometimes called Z in the demand-led growth literature. Z comprises exogenous government spending, autonomous household consumption expenditure, some forms of private investment that do not directly create capacity (notably, research and development) and, for open economies, export demand. The significance of this category of demand is that it promotes fuller capacity utilization. It boosts demand and income both directly and through its multiplier effects relative to productive capacity, which it does not directly affect.

The growth rate of Z helps to define a rate of output growth to which the economy notionally tends. In the special case of a stable normal output to capital ratio, Z is the sole determinant of the economy’s trend growth rate. More generally, the growth rate of Z together with changes in the normal output to capital ratio (q) jointly determine the trend growth rate. While the economy will notionally be drawn by the trend, in reality the convergence process never completes because, even for a given q: (1) the growth rate of Z never remains constant for long enough for full adjustment to occur, and (2) even if the growth rate of Z did remain constant for a long time, the marginal propensities to consume, tax, save, and import, though fairly stable, are not strictly constant.

To bring out the suggested ‘demand led’ causation, however, it helps to begin with a stylized scenario. Suppose that q (the normal output to capital ratio) is stable while Z, private investment and the economy as a whole all grow at a constant rate of 1 percent per annum, with firms operating at their planned or normal rates of capacity utilization. The economy will be in a steady state (growing at a constant rate) and fully adjusted position (normal capacity utilization).

Suppose, now, that the growth rate of Z jumps to 2 percent, and remains there, while initially the growth rate of private investment remains at 1 percent. Through the direct and multiplier effects of the more rapid growth in Z, total output will rise relative to private-sector productive capacity, causing the rate of capacity utilization to increase, taking it above normal. If the effect is persistent, and the normal rate of profit exceeds the minimum necessary for private investment to be feasible, firms will be induced to accelerate private investment in an attempt to restore capacity utilization to normal.

At first, the accelerated private investment reinforces the rise in capacity utilization, because the direct demand effect of private investment is immediate whereas the capacity effect takes time. The accelerated private investment also has multiplier effects, further stimulating demand. But at a certain point, once new capacity comes on line, the change in the rate of utilization, and then the rate of utilization itself, will shrink, eventually causing capacity utilization to fall below normal, discouraging private investment. There will be a deceleration (and possible slump) in private investment.

Nevertheless, if Z continues to grow at the rate of 2 percent per annum, total output will once again mount relative to capacity, and the rate of utilization will once again rise toward and then beyond normal, setting off a repeat of the cyclical process.

What has just been described is a demand-led investment process predicated on normal profitability acceptable to capitalists. The trend growth rate is set by the behavior of Z (and, more generally, q) whereas the cycles around that rate are driven by the behavior of private investment. These cycles are not usually seriously problematic for capitalism. The serious problem for capitalism comes once normal profitability falls too low to justify private investment. The cause of this will be a rising organic composition of capital, which corresponds to a falling normal output to capital ratio (a falling q). When q, rather than remaining stable, declines over an expansionary phase of capitalist accumulation, the normal rate of profit tends to fall. Once r falls below rmin, a crisis is functionally necessary to restore normal profitability. Although the immediate catalyst for the crisis is likely to be something else, such as a financial crisis, Marx’s theory suggests that failing profitability will be the underlying cause, prompting an increasing resort to speculative or unsustainable behavior in a futile attempt to overcome the lack of profitability in production.

Remark 5 – Capacity utilization and actual profitability

Although the demand-led capitalist accumulation process is based on a positive relationship between private investment and the rate of capacity utilization, it also implies – other factors remaining equal – a positive relationship between private investment and the actual, observable rate of profit.

By identity, the actual rate of profit, adjusted for inflation, can be decomposed into the product of three terms – the profit share in income p, the utilization rate u, and the normal output to capital ratio q – such that ra = puq. For given ‘distribution’ p and ‘technology’ q, the actual rate of profit and rate of capacity utilization move together.

Marx’s theory, however, suggests that q will fall as capitalists accumulate. If so, ra and u will not necessarily move together (depending on the behavior of p). While above normal rates of capacity utilization still support actual profitability in these circumstances, the fuller capacity utilization also encourages accelerated investment, which, according to Marx, reinforces the decline in q, and this ultimately hurts both actual and normal profitability.

The rate of profit that matters for the long-term viability of private investment is the normal rate. This is the profit rate associated with normal capacity utilization. If the actual rate of utilization is defined as u = Y/Yn, where Y and Yn are actual and normal output, normal capacity utilization occurs when actual output equals normal output; that is, when u = 1. The actual rate of profit, ra = puq, will then equal the normal rate r = pq.

Remark 6 – Behavior of the normal rate of profit

The long-term behavior of the normal rate of profit, r = pq, depends on ‘distribution’ (the profit share in income p) and ‘technology’ (the normal output to capital ratio q).

The ratios p and q can be related to Marx’s categories in which c is constant capital, v variable capital, s surplus value, and C total capital. Movements in p (the profit share in income) tend to be in the same direction as movements in the rate of surplus value, since p loosely corresponds to s/(v+s), which moves in the same direction as s/v. Movements in q (the normal output to capital ratio) tend to be in the opposite direction to movements in the composition of capital, since q roughly corresponds to (v+s)/C, which moves in the opposite direction to C/v and c/v for given v and s.

Marx argues in chapter 13 of the third volume of Capital that the technical and organic compositions of capital tend to rise (and, by implication, q tends to fall) over an expansionary phase of capitalist accumulation. This tendency is driven by the quest for productivity improvements, which enable a given workforce, in the same time, to work more machinery and process more raw materials. The mass of constant capital (‘real’ c) tends to increase relative to productive employment (‘real’ v). The value composition of capital also tends to rise unless the prices of the elements of constant capital fall sufficiently to offset the quantity effects, which Marx considers unlikely so long as the system is in expansionary mode. To the extent that the composition of capital rises (or the normal output to capital ratio q falls), the normal rate of profit is depressed.

One of the ‘counteracting tendencies’ discussed by Marx in chapter 14 of the same volume is the possibility of a rise in the rate of surplus value (which would imply a rise in the profit share p). He points out, though, that since an increase in the rate of surplus value is primarily achieved through productivity improvements, and these tend to be achieved through a rising composition of capital, this avenue for preventing a fall in the normal rate of profit has limitations. If it turns out that movements in p are insufficient to counter (over an expansionary phase of capitalist accumulation) a fall in q, the normal rate of profit will decline, bringing the possibility that the minimum rate of profit necessary for a demand-led process of private investment is not forthcoming. In that event, for capital accumulation to be rejuvenated, there needs to be a collapse in capital values. This, while resulting in severe losses on existing capital, revives the rate of profit applying to new investments. The revival of the normal rate of profit, together with adequate demand, will be sufficient for a recovery in private investment.

Remark 7 – Marx on the impetus to invest (and employ) amid falling profitability

Marx, consistent with what has been assumed here, held that profit is the overriding motive of capitalist production:

It is the rate of profit that is the driving force in capitalist production, and nothing is produced save what can be produced at a profit. (Capital, Vol. 3, pp. 368, Penguin, London)

He did not, however, argue that private investment will weaken in the face of a falling profit rate, provided investment remains profitable (characterized here as r > rmin):

A fall in the profit rate, and accelerated accumulation, are simply different expressions of the same process, in so far as both express the development of productivity. Accumulation in turn accelerates the fall in the profit rate, in so far as it involves the concentration of workers on a large scale and hence a higher composition of capital. On the other hand the fall in the profit rate again accelerates the concentration of capital, and its centralization, by dispossessing the smaller capitalists and expropriating the final residue of direct producers who still have something left to expropriate. In this way there is an acceleration of accumulation as far as its mass is concerned, even though the rate of this accumulation falls together with the rate of profit. (Ibid, p. 349)

Marx’s argument here is consistent with a view that capitalist firms will be driven to invest despite a falling rate of profit. In Marx’s theory, it is in fact the accumulation process that causes the rate of profit to fall. Capitalists accumulate, despite the falling profitability, because their survival depends on it. Technical advances and productivity improvements that temporarily enable individual firms to outcompete their rivals ultimately depress the rate of profit once the advances and improvements are generalized and adopted by other firms.

The impetus to invest also has implications for employment:

The number of workers employed by capital, i.e. the absolute mass of labour it sets in motion, and hence the absolute mass of surplus labour it absorbs, the mass of surplus-value it produces, and the absolute mass of profit it produces, can therefore grow, and progressively so, despite the progressive fall in the rate of profit. This not only can but must be the case – discounting transient fluctuations – on the basis of capitalist production. (Ibid, p. 324)

Marx never undertook a full analysis of government spending, or of the role of autonomous demand more generally, but the following passage on foreign trade applies equally to government spending. I have inserted numbering for easy reference.

In so far as foreign trade [1] cheapens on the one hand the elements of constant capital and on the other [2] the necessary means of subsistence into which variable capital is converted, it acts to [3] raise the rate of profit by raising the rate of surplus-value and reducing the value of constant capital. It has a general effect in this direction in as much as it permits [4] the scale of production to be expanded. In this way it accelerates accumulation, while it also accelerates the fall in the variable capital as against the constant, and hence the fall in the rate of profit. And whereas the expansion of foreign trade was the basis of capitalist production in its infancy, it becomes the specific product of the capitalist mode of production as this progresses, through the inner necessity of this mode of production and [5] its need for an ever extended market. (Ibid, p. 344)

Just as foreign trade can [1] cheapen elements of constant capital, government spending on public infrastructure and basic research does the same. Just as foreign trade can [2] cheapen wage goods, government spending on schools, hospitals, public transport, and so on, reduces the total cost of culturally reproducing workers. These effects [3] bolster the rate of profit by lowering the value of constant capital and raising the rate of surplus value. Government spending, like foreign trade, facilitates [4] an expansion of the scale of production by constituting an independent, autonomous source of demand for the products of capitalist production and so meets the need of the capitalist mode of production for [5] an ever extended market.

None of these considerations remove the ultimate limit on capitalist accumulation, which is the possibility that the normal rate of profit eventually falls below the rate deemed viable by capitalists. It just means that the demand-led private-investment process will function so long as that limit is not breached. If and when it is breached, crisis is functionally necessary to revive profitability and reactivate the demand-led process. Crisis is the solution offered within the internal logic of capitalist accumulation.

Remark 8 – Sketch of a simple model for illustrative purposes only

A simple model may help to illustrate the demand-led private-investment process just described. Though just a sketch, it will give a basis for a graphical depiction of the process in the following remark.

Consider the system:

Y is income. Yd is demand. DI is endogenous demand. α is the marginal propensity to leak to taxes, saving and imports, assumed constant. I is private investment, specified below. Z is autonomous non-capacity-creating demand, which equals exogenous government spending net of autonomous taxes, plus autonomous private household consumption expenditure, plus exogenous exports net of exogenous imports.

Solving (1) for Y gives equilibrium income:

It is possible to distinguish actual and equilibrium income, but to keep things simple this will not be done here. It should be kept in mind, though, that equilibrium income does not imply a fully adjusted position. The latter only occurs when output is at its normal level (Y = Yn), corresponding to normal capacity utilization (u = 1). Equilibrium income just means that current output is adjusted to current demand, which can occur at any feasible rate of utilization.

The expression for equilibrium income implies that the growth rate of income is a weighted average of the exogenously given growth rate of Z and the growth rate of private investment:

A change in the exogenous growth rate of Z will cause the growth rate of income to change, which, by altering capacity utilization, will have subsequent effects on the growth rate of investment and the share of investment in autonomous demand, causing further interaction between the variables.

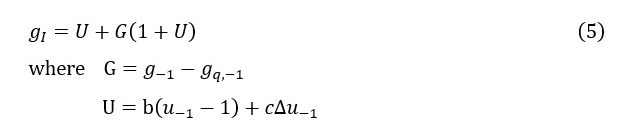

Private investment, while being treated here as autonomous of current-period income, is induced by recent movements in the level of activity and technology provided the normal rate of profit remains acceptable to capitalists:

The coefficients b and c are small positive constants. So long as the normal rate of profit is at least minimally acceptable, private investment depends on the growth rate of income, the growth rate of the normal output to capital ratio, the divergence of the actual rate of utilization from its normal rate, and the change in the actual rate of utilization, all lagged one period. Private investment also depends on its own level in the previous period. If the normal rate of profit falls below rmin, it is assumed that investment ‘collapses’ to some constant positive multiple χ of the previous period’s investment.

On the basis of the investment function,

Private investment grows faster or slower than G according to the sign of U.

Investment enables an adaption of normal output Yn to demand through increments in the capital stock K. Lagging the capacity effect of investment one period and assuming a constant rate of depreciation δ,

The growth behavior of Yn depends partly on K and partly on q. If q in the current period is a constant fraction of its value in the previous period,

Stable q requires k = 1. Marx’s profit-rate tendency comes into play when k < 1.

On the basis of (6) and (7), normal output and the capital stock grow according to

Concealed in (8) is an implication concerning the investment share in income. For a given growth rate of Z, a falling normal output to capital ratio requires a rising investment share in income. This can be seen by noting that a particular growth in normal output (a particular gn) requires sustaining a particular growth in the capital stock (a particular gK). By writing I/K as (I/Y)(Y/Yn)(Yn/K) = huq, the growth rate of the capital stock takes the form gK = h-1u-1q-1 – δ. Since δ is constant and u tends to one, maintaining a particular gK alongside a falling q (in order to maintain the desired gn) requires a higher investment share in income (a higher h-1).

This is connected to the tendency, in Marx’s analysis, for capitalist accumulation to raise the composition of capital and lower the normal rate of profit. Eventually, if the process continues long enough, the normal rate of profit falls below the minimum rate acceptable to capitalists. A renewal of accumulation on a capitalist basis then requires a revival in profitability. A crisis revives profitability by lowering the composition of capital. This mainly occurs through a devaluation of capital but can also involve a destruction or abandonment of real capital (especially if war is involved).

To account for the functional role of crises in reviving the normal rate of profit, we need to separate out price and quantity effects. Let pO and pK be indices of output and input prices, respectively. The actual and normal rates of profit can then be expressed in nominal terms:

For simplicity, p and pn (the ‘real’ and ‘nominal’ profit shares in income) are assumed constant. In terms of Marx’s tendential fall in the profit rate, a rise in the profit share would be a counteracting tendency; its fall, a reinforcing one. Holding the profit share constant enables the focus to be on what Marx regarded as the main factor affecting the normal rate of profit, namely the behavior of the composition of capital, here reflected in the behavior of q and qn.

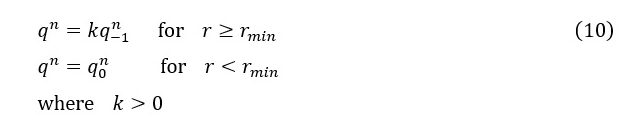

To isolate this behavior, suppose that all prices are stable in expansions but that the prices of the elements of fixed capital collapse in crises. (The key assumption is simply that crises cause fixed capital to devalue relative to output.) The assumed price behavior means that a falling q translates into a falling qn during expansions but that qn can be revived in crises (here to its original value):

For k < 1, what results is a succession of demand-led capitalist growth ‘eras’ in which the economy expands for a time until a crisis becomes functionally necessary to revive profitability. So long as the growth rate of Z remains adequate, the revival of profitability enables a new era of capitalist accumulation.

Remark 9 – A graphical illustration

The model just sketched can be used to construct various scenarios. The scenario considered here is based on a particular set of parameter values.

Assorted values. The marginal propensity to leak is 0.5, half of which goes to taxes. Initially, Z is 30, private investment is 20, output and normal output are 100, the rate of utilization is one, its change is zero, and the real capital stock is 200. The exogenous growth rates of Z and q are 0.02 and -0.005, respectively. The investment parameter values are b = 0.1 and c = 0.5. The rate of depreciation, applied on the basis of historical cost, is 0.07.

Price Indices. The price indices for output and inputs both start at one. However, with each crisis, the price index applying to inputs falls so as to reset the nominal value of the normal output to capital ratio (qn). Specifically, the pre-crisis price index is multiplied by the most recent qn (0.44 in the illustration) and divided by the original qn (0.5). This means, in the present scenario, that the price index gets multiplied by 0.88 each time there is a crisis, then remains constant at that level until the next crisis.

Rate of profit. The profit share in income (p) is fixed at 0.25. The normal output to capital ratio (q) starts at 0.5. (Initially, both q and qn are 0.5.) Therefore, the after-tax normal rate of profit (before distribution into industrial profit, interest, rent, and other forms) starts at 0.125. Accumulation causes q and qn to fall (their values in one period are 0.995 of their values in the previous period) which, in turn, causes the normal rate of profit to fall until it hits rmin, arbitrarily set at 0.11. This provokes a crisis in which investment ‘collapses’ to 0.97 of its previous level and qn (but not q) is reset to 0.5, reviving the normal rate of profit.

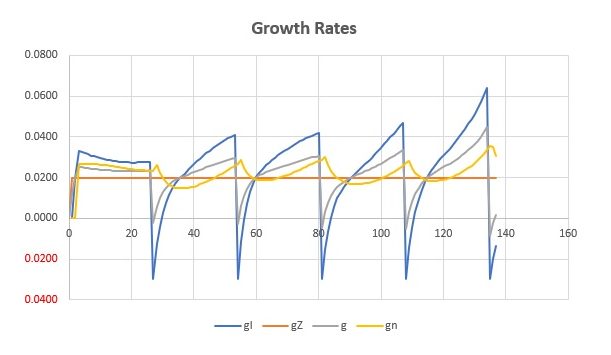

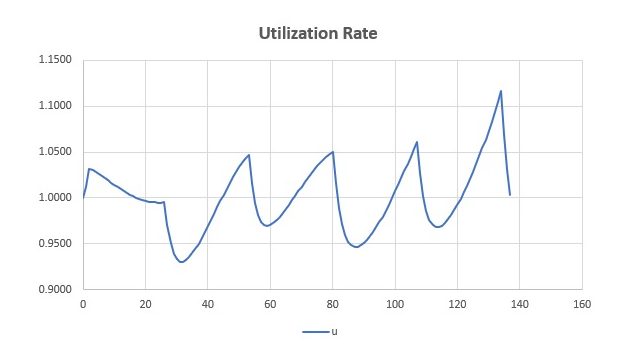

Graphs. The first figure shows the trajectory of output, normal output, private investment and non-capacity-creating autonomous demand over the entire ‘history’ of the scenario. Ymax is the maximum possible output that technically could be produced. If output hit up against this technical maximum, there would be pure inflation, non-price rationing, or some combination of the two. Real capitalist economies usually stay well within the ultimate capacity limit. An average Y/Ymax of 0.8 is quite typical, and that is the case in the illustration economy with an average ratio of 0.8005.

The average growth rates of output (0.0220), normal output (0.0220) and private investment (0.0244) are lifted by the positive exogenous growth rate of Z (0.0200). When the normal output to capital ratio is falling, as it is here, the endogenous variables outpace Z. The growth of private investment is more volatile than the growth of other variables and drives the economy’s cyclical fluctuations.

The attempt by firms to adjust capacity to demand means that the average utilization rate over the entire history is very close to one (1.0007), the average change in utilization is very close to zero (0.0000 to four decimal places), and the average U is very close to zero (0.0002). In theory, these figures should be exactly one, zero and zero, respectively, on the average.

In between crises, the normal rate of profit falls steadily due to the decline in the normal output to capital ratio at the constant rate of minus half a percent. The actual rate of profit sometimes bucks the trend and sometimes falls more sharply than the normal rate because of positive and negative fluctuations in the rate of capacity utilization.

The long-term effect of a falling normal output to capital ratio on the private investment share in income is evident in the final figure. The technical change means that more investment (a larger increment in the real capital stock) is needed to achieve a desired adjustment of normal output to demand. Given adequate demand, the greater technical requirement will spur more rapid investment and cause the investment share in income to rise. When autonomous non-capacity-creating demand grows at the scenario’s base rate of two percent, the investment share rises by about seven percent. The investment share only rises by about two percent if the growth rate of autonomous demand is instead set lower at one percent.

Remark 10 – Summary of the private-investment process and its preconditions

To sum up the main aspects of demand-led growth, the combined behavior of autonomous non-capacity-creating demand (Z) and the normal output to capital ratio (q) determines the trend rate of growth while private investment behavior causes fluctuations around that rate. In the couple of decades leading up to the global financial crisis of 2007 and Great Recession of 2008, for instance, there was strong growth of autonomous household consumption expenditure. This was the main driver of Z and, under the causation described above, would have helped, along with its multiplier effects, to promote fuller capacity utilization and induce private investment. However, the growth in autonomous household consumption expenditure was dependent on an unsustainable buildup of private debt. Unlike currency-issuing governments, households as currency users are financially constrained.

A currency-issuing government is better placed to sustain growth in Z. If it does so on an ongoing basis, it can help to induce private investment so long as the normal rate of profit remains acceptable to capitalists. Once the normal rate of profit falls below this level, government spending can help to ensure that, once profitability revives through crisis, demand is no obstacle to a recovery in private investment.

In other words, government spending can support capital accumulation. But if Marx’s profit-rate law is operative, there will still be a functional need for periodic crises to revive profitability, crises that have negative economic and social consequences. These crises would be unnecessary in a more rational (and humane) system.

Remark 11 – The inappropriateness of relying on private investment

While persistent growth in government spending in combination with periodic crises can underpin demand-led capitalist growth, a reliance on this process is unlikely to deliver the significant changes in consumption, investment and production that are needed to overcome our present challenges. Especially in the context of an ecological crisis, both requirements of private investment – a normal rate of profit acceptable to capitalists and adequate growth in demand – are problematic.

The profitability of doing what needs to be done, while being a precondition of private investment, is an irrelevant criterion from a society-wide perspective. If we are to survive, what needs to be done will need to be done, with or without profitability.

Maintaining demand at the levels necessary to drive private investment is also problematic if it comes with ecological costs that could be avoided through a low-growth, no-growth, or degrowth strategy. An aspect of MMT’s proposed job guarantee that is critically important when it comes to ecological concerns is that full employment can be maintained irrespective of the overall level of demand and rate of growth. Likewise, a critically important aspect of public investment, viewed in the same respect, is that it can occur irrespective of the overall level of demand and rate of growth.

Starting from our present position, and in view of existing political realities, in all likelihood the policy approach will involve a mix of public and private investment. If so, the latter will need to operate within a modified incentive and regulatory framework. It is hard to expect much progress, however, unless there is a pronounced shift away from for-profit activity and toward public sector and other not-for-profit production; a move away from marxian value creation to a system based on directly social labor.

MMT in my view is important, above all, because it shows that currency-issuing government has the technical capacity to effect this transition. The fact that a currency-issuing government always has the capacity to purchase whatever is available for sale in its currency means that it always has the capacity to undertake or support not-for-profit activity through utilization of whatever resources the for-profit private sector opts to leave idle. It is not necessary to dismantle the existing monetary system before turning to this task. The challenge at the grassroots level is to develop the collective will for such a transition and to express it effectively in industrial and political spheres.